OT: Lets talk about stocks (Part 3)

- Thread starter Lshap

- Start date

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

- Status

- Not open for further replies.

Quatre Vingt Treize

Registered User

It bounced back .75 cents. I figured it would. Noticed past dividend dates. So i gained around $410 waiting extra day. Not much but days pay. It was Royal Bank. On Ex-date, the 25th, it dropped from $131 to $129.85. I sold today for $130.60.Theoretically the dividend and dividend date shouldn't factor into your evaluation to buy/sell because that dividend (barring any kind of massive announcement) is already factored into the stock price. If there are any market inefficiencies to take advantage of then investment firms and hedge funds have the tools to do so a hell of a lot quicker and more efficiently than us retail joe blows. I think you're better off just holding through personally, but to each their own.

montreal

Go Habs Go

Do Valuations Even Matter For the Stock Market? - A Wealth of Common Sense

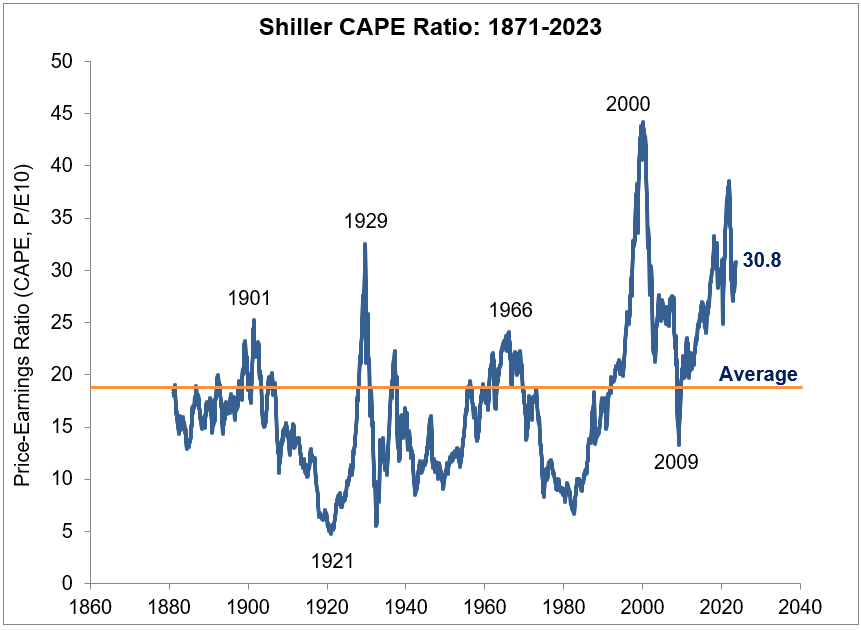

Robert Shiller has a free online database of historical stock market data I’ve been using for years. Going back to 1871, Shiller has data on historical interest rates, dividends, earnings, inflation and valuations. His preferred valuation measure is the cyclically-adjusted price to earnings...

awealthofcommonsense.com

awealthofcommonsense.com

Quatre Vingt Treize

Registered User

Quatre Vingt Treize

Registered User

Been watching AMC stock episode unfold this week. Trying to figure a way to make money. But could be the end for theatres. AMC racked up so much debt during covid I have my doubts they ever get back.

AMC did a 10:1 reverse stock split, early as Monday they are allowed to release up to 550 million new shares to raise capital. It is smart move but I have doubts AMC will survive. People just don't seem to go to movies like they once did. The box office hits will draw like pre-covid era, but doubt they enough for AMC to survive long term. Costs a lot of money to operate a theatre. Hope I am wrong. August been a bad month on stock market. There is a writers strike going on also. Both never helped.

Most People have big screen TVs in their homes now. With online streaming and Netflix, YouTube, so many areas for entertainment. Going to a movie is expensive also If AMC goes under going to be hard to see theatres go.

AMC did a 10:1 reverse stock split, early as Monday they are allowed to release up to 550 million new shares to raise capital. It is smart move but I have doubts AMC will survive. People just don't seem to go to movies like they once did. The box office hits will draw like pre-covid era, but doubt they enough for AMC to survive long term. Costs a lot of money to operate a theatre. Hope I am wrong. August been a bad month on stock market. There is a writers strike going on also. Both never helped.

Most People have big screen TVs in their homes now. With online streaming and Netflix, YouTube, so many areas for entertainment. Going to a movie is expensive also If AMC goes under going to be hard to see theatres go.

Quatre Vingt Treize

Registered User

The AMC debacle continued yesterday. Smashed again, dropped to $8.85 a share. Which is really .86 cents a share.. Interesting to see how this unfolds. Is it over bestup? Will it go under? Will America give up their theatres as we know it?

They going to release 40 million more shares. But at $8-9 bucks a share that's only 350 million. Peanuts on a 9.5 debt. The Taylor Swift thing not enough to save AMC

They going to release 40 million more shares. But at $8-9 bucks a share that's only 350 million. Peanuts on a 9.5 debt. The Taylor Swift thing not enough to save AMC

Quatre Vingt Treize

Registered User

Apple’s first investor was Mike Markkula.

He put in $250,000 for 1/3 of the business.

Today, 1/3 of Apple is worth $930 billion.

He put in $250,000 for 1/3 of the business.

Today, 1/3 of Apple is worth $930 billion.

Quatre Vingt Treize

Registered User

Reading yup, increases knowledge. Experience most important thing in stock market I found.

Years ago I said to myself, everybody knows there's tons of money in stock market. But need to figure it out. Most I find rush in, think they know it all, get burned and quit. Too gung-ho. Takes time. That first year Tesla jumped way up I made $400,000. The next year I made $200,000. First year of covid. These last 21 months, I maybe broken even.

DAChampion

Registered User

- May 28, 2011

- 30,551

- 24,100

I wonder if we'll ever see cars sell for MSRP again.

The norm now is for cars to have a lot of useless upgrades and have a "market adjustment fee". 20% above MSRP is probably typical.

The norm now is for cars to have a lot of useless upgrades and have a "market adjustment fee". 20% above MSRP is probably typical.

calder candidate

Registered User

Will see price adjust down when people stop paying, dealers ship are taken advantage of perceived shortage in supply to get paying for stuff that the didn’t want or need because that where they make their most of their profit.I wonder if we'll ever see cars sell for MSRP again.

The norm now is for cars to have a lot of useless upgrades and have a "market adjustment fee". 20% above MSRP is probably typical.

- Jun 24, 2012

- 84,318

- 166,876

If you can put money in a GIC for one year and garner over 5.5% interest, is it really worth investing in the stock market at this time?

Sample best rates currently: Best GIC Rates in Canada - NerdWallet

Also, which is more likely to net a higher return (after transaction costs and fees) — buying index funds or mutual funds?

Sample best rates currently: Best GIC Rates in Canada - NerdWallet

Also, which is more likely to net a higher return (after transaction costs and fees) — buying index funds or mutual funds?

montreal

Go Habs Go

If you can put money in a GIC for one year and garner over 5.5% interest, is it really worth investing in the stock market at this time?

Sample best rates currently: Best GIC Rates in Canada - NerdWallet

Also, which is more likely to net a higher return (after transaction costs and fees) — buying index funds or mutual funds?

it comes down to several factors. 5.5% but minus taxes + inflation. So if you want to avoid risk then for sure, but if you are young I would look at something more aggressive.

That said in this current climate, I wouldn't blame anyone that just put money under their mattress since their are so many issues with the US-China/Russia and a possible WWIII threat that these assholes keep pushing us closer to.

On the other hand no one seemed ready for the AI boom, I mean I had a decent amount of Nvida before the crazy run it's on but holy shit is that crazy how much money they are making now from AI (20B in 6 months I believe). So the talk is that it could have a bigger impact on the market then the internet did in the '90's (I don't believe it will be even half as big though as I traded back then and it was nuts)

Index vs mutual fund and I would add ETF's since they are the same thing just about, again it depends on your risk tolerance and what you want. I started out at The Vanguard Group out of college so you can't go wrong with buying the S&P 500 index and sitting on it for 20 years or so.

- Jun 24, 2012

- 84,318

- 166,876

Thx for that, while I know I can’t time the market, I’m looking to jump in on an ETF or mutual funds on a major downturn.it comes down to several factors. 5.5% but minus taxes + inflation. So if you want to avoid risk then for sure, but if you are young I would look at something more aggressive.

That said in this current climate, I wouldn't blame anyone that just put money under their mattress since their are so many issues with the US-China/Russia and a possible WWIII threat that these assholes keep pushing us closer to.

On the other hand no one seemed ready for the AI boom, I mean I had a decent amount of Nvida before the crazy run it's on but holy shit is that crazy how much money they are making now from AI (20B in 6 months I believe). So the talk is that it could have a bigger impact on the market then the internet did in the '90's (I don't believe it will be even half as big though as I traded back then and it was nuts)

Index vs mutual fund and I would add ETF's since they are the same thing just about, again it depends on your risk tolerance and what you want. I started out at The Vanguard Group out of college so you can't go wrong with buying the S&P 500 index and sitting on it for 20 years or so.

I’m not a fan of investing in individual stocks unless it’s blue chips, but I’ve been reading very favourable comments on Palantir and will take a position when some funds become available. Has this stock been on your radar of late?

montreal

Go Habs Go

Thx for that, while I know I can’t time the market, I’m looking to jump in on an ETF or mutual funds on a major downturn.

I’m not a fan of investing in individual stocks unless it’s blue chips, but I’ve been reading very favourable comments on Palantir and will take a position when some funds become available. Has this stock been on your radar of late?

If you like some risk, I have done well with 2 ETF's, BOTZ and BETZ. I had SLV too as something very shady is going in with the price of Silver so I got out.

I picked up Palantir and PATH after doing real well with symbol Ai, which I dumped a few weeks back to start a position in both of these. I didn't buy too much as I wait to see what happens (the sector was red hot so I expect it to cool at bit) if it drops a good bit then I will add more, if not then we'll see how it goes but of course I trade for a living so I don't suggest anyone do what I do.

japhi

Registered User

- Jul 7, 2014

- 3,713

- 3,133

Unless on fixed income, and even then, I'm not a fan of GIC in an environment where there is is lots of risk, anc real inflation is running 5%+. You basically aren't making anything net inflation, they aren't a tax friendly investment vehicle, and if this market does pop, you want to be as liquid as possible. Look how quick markets recovered during COVID.If you can put money in a GIC for one year and garner over 5.5% interest, is it really worth investing in the stock market at this time?

Sample best rates currently: Best GIC Rates in Canada - NerdWallet

Also, which is more likely to net a higher return (after transaction costs and fees) — buying index funds or mutual funds?

You are better off in a HISA. I bank with TRD so TDB8150, full liquid, interest calculated daily, and pays 4.55%.

There is some stuff on sale, stuff like ENB that T that pay 6-8% divvies and are near 52 week lows. Not withoiut risk but should do well long term/

FWIW I think a big economic event is on the horizon so I am 20%+ cash. HISA great way to make a few bucks while waiting, and some good buys on boring stuff if you have the time to do the research. I mean the SP 500 is up 15% YTD so little reason to be in GIC's IMO

montreal

Go Habs Go

Unless on fixed income, and even then, I'm not a fan of GIC in an environment where there is is lots of risk, anc real inflation is running 5%+. You basically aren't making anything net inflation, they aren't a tax friendly investment vehicle, and if this market does pop, you want to be as liquid as possible. Look how quick markets recovered during COVID.

You are better off in a HISA. I bank with TRD so TDB8150, full liquid, interest calculated daily, and pays 4.55%.

There is some stuff on sale, stuff like ENB that T that pay 6-8% divvies and are near 52 week lows. Not withoiut risk but should do well long term/

FWIW I think a big economic event is on the horizon so I am 20%+ cash. HISA great way to make a few bucks while waiting, and some good buys on boring stuff if you have the time to do the research. I mean the SP 500 is up 15% YTD so little reason to be in GIC's IMO

I manage money (less then 1M) and have been sitting between 25-30% cash. I have thought about going 40-60% soon though.

Lafleurs Guy

Guuuuuuuy!

- Jul 20, 2007

- 75,719

- 60,201

I have thrown a good potion into GICs for a year. Might as well preserve some buying power until the market sorts itself out. 5 and a half percent is a good guarantee these days.I manage money (less then 1M) and have been sitting between 25-30% cash. I have thought about going 40-60% soon though.

Quatre Vingt Treize

Registered User

Exactly what I am debating right now. If China invades Taiwan, or nuclear war breaks out in Russia, it will crush the stock market. I should go have and have. Equities and fixed income. I think 50/50 chance one of those will happen. If S&P jumped over 4,500 today I was thinking sell out.If you can put money in a GIC for one year and garner over 5.5% interest, is it really worth investing in the stock market at this time?

Sample best rates currently: Best GIC Rates in Canada - NerdWallet

Also, which is more likely to net a higher return (after transaction costs and fees) — buying index funds or mutual funds?

japhi

Registered User

- Jul 7, 2014

- 3,713

- 3,133

In a similar boat, just checked I'm at 22%. May sell some dogs to get to 30%.I manage money (less then 1M) and have been sitting between 25-30% cash. I have thought about going 40-60% soon though.

Recent history shows that post economic event, the Govt steps in, over corrects and markets recover in months. COVID, the SP500 took two months to bottom, and only 4 months to recover to pre Covid levels.

Have to be quick and those holding GICs may miss the whole correction. The Delta between a GIC and HISA - about 75bps, and then the delta between a GIC and the SP500 - about ten points YTD, makes GICs pretty unattractive.

I'm not concerned with those items as much as the massive credit bubble. Our economy is built on consumer spending and the Consumer is evaporating. If and when RE finally corrects in a meaningful way, and Amorts are held at 25 years on renewal, look out. Your neighbors can't actually afford that house, the two new vehicles and the trips to Mex without free and widely available credit.Exactly what I am debating right now. If China invades Taiwan, or nuclear war breaks out in Russia, it will crush the stock market. I should go have and have. Equities and fixed income. I think 50/50 chance one of those will happen. If S&P jumped over 4,500 today I was thinking sell out.

Quatre Vingt Treize

Registered User

Where interest rates have jumped you mean, combined with so much consumer debt? Heard that stuff since I was in grade 10 economics class, circa 1979 though.I'm not concerned with those items as much as the massive credit bubble. Our economy is built on consumer spending and the Consumer is evaporating. If and when RE finally corrects in a meaningful way, and Amorts are held at 25 years on renewal, look out. Your neighbors can't actually afford that house, the two new vehicles and the trips to Mex without free and widely available credit.

Look at 10 year treasury rates? Crazy high, highest it's been in 15 years. Yet the market when up today. Should never happened? Equities Been on decent run since May. Has to be something pushing it.

japhi

Registered User

- Jul 7, 2014

- 3,713

- 3,133

Banks are extending amortizations over 35 years to allow variable rate holders that can't afford the payment the ability to stay in their house until the term is up. If Amorts don't change, and OSFI enforces the new high LTV rules (OSFI proposes changes to manage mortgage risks, preserving access for Canadians) then this whole house or cards will eventually fall apart. And fast....highly leveraged homeowners will go from being able to just make payments, to having to list to sell, to finding they are underwater with no market to sell into, and ultimately bankrupt. Only takes a few guys s in a neighborhood that need to sell, to take the market down 30%. Once that happens, housing corrects, party is over.Where interest rates have jumped you mean, combined with so much consumer debt? Heard that stuff since I was in grade 10 economics class, circa 1979 though.

Look at 10 year treasury rates? Crazy high, highest it's been in 15 years. Yet the market when up today. Should never happened? Equities Been on decent run since May. Has to be something pushing it.

Also, September inflation print in Canada is going to be north of 3.5%, possibly 4%. Rates are going to have to go up, or we will need to accept entrenched inflation. We are in this crazy scenario whereby interest rates are the largest driver of inflation, yet they need to continue to go up to kill consumer spending. Canadians are financially illiterate - credit balances are increasing FFS - I suspect most people have no idea what comes next.

Edit: this link shows what's happening with consume credit while we are at full employment. Imagine what the numbers will look like in a recession with 7% UI:

Press Releases | About Us | Equifax Canada

Search our press releases on everything from identity theft to credit scores, credit reports and more.

www.consumer.equifax.ca

www.consumer.equifax.ca

LyricalLyricist

Registered User

If you can put money in a GIC for one year and garner over 5.5% interest, is it really worth investing in the stock market at this time?

Sample best rates currently: Best GIC Rates in Canada - NerdWallet

Also, which is more likely to net a higher return (after transaction costs and fees) — buying index funds or mutual funds?

Unpopular opinion but if an investor doesn't know what they are doing or can't afford risk there is nothing wrong with a GIC. Yes, you may just cancel out inflation but its better to make 5% than lose it.

My personal opinion though is to throw these into TFSA because at least its guaranteed 5% after taxes and guaranteed growth in TFSA contribution room.

But you do what you want. The idea is to invest based on your risk tolerance.

- Status

- Not open for further replies.

Latest posts

-

GDT: WCF | II | "Stay Outta The" | Oilers @ Stars | "Box" | 5.21.25 | 6:00PM | SN (166 Viewers)

- Latest: stewy04

-

New York Islanders: Mathieu Darche is named GM of the New York Islanders (44 Viewers)

New York Islanders: Mathieu Darche is named GM of the New York Islanders (44 Viewers)- Latest: impaaaaaact

-

GDT: [WCF R3 GM2] Dallas Stars vs. Edmonton Oilers – 7:00 PM CT (ESPN+/CBC) (178 Viewers)

GDT: [WCF R3 GM2] Dallas Stars vs. Edmonton Oilers – 7:00 PM CT (ESPN+/CBC) (178 Viewers)- Latest: ChaoticOrange

-

News Article: NCC putting in a lot of conditions for the downtown site (11 Viewers)

News Article: NCC putting in a lot of conditions for the downtown site (11 Viewers)- Latest: Stylizer1

-